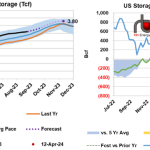

For the storage week ending August 25th, the EIA reported a net injection of 32Bcf. With the South Central U.S. region again posting the only decrease, withdrawing 22 Bcf. This brings working gas storage to 3,115 Bcf. Stocks are 484 Bcf higher than this time last year and 249 Bcf above the 5-year average. This report follows one of the most bullish storage reports this season of a net 18 Bcf injection.

Featured Articles

- Analyst Insight

TTF Futures Rally Following Strike Concerns in Australia

TTF Futures Rally Following Supply Concerns.

- Blog

What's Going On? - Bullish EIA Storage Report Signals a Big Shift in the U.S. Natural Gas Market

The U.S. Energy Information Administration (EIA) on Thursday (June 9) reported a surprisingly bullish 65-Bcf injection for the week ended June 3—that was 8.0 Bcf below our Natgas Billboard estimate and more than 10 Bcf below the Bloomberg industry average assessment. In response, the CME/NYMEX Henry Hub July natural gas contract screamed about 15 cents higher following the report to a settle of $2.617/MMBtu, the highest daily settle for the prompt month in nearly 9 months. Thursday’s gains extended a rally that began on May 31 (2016) just after the July contract rolled to the front of the futures curve. It’s likely the rally was initially spurred by market participants looking to cover their short positions. But in the past week, an increasingly bullish fundamental picture has emerged prompting us to raise our price outlook (in our June 10 NATGAS Billboard report). In today’s blog, we analyze the fundamentals behind rising natural gas prices.

- Blog

Razor's Edge - Tight Supply-Demand Balance Brings Back Natural Gas Price Volatility

Volatility is back big time in the U.S. natural gas market. The CME/NYMEX Henry Hub prompt natural gas futures contract in mid-November raced up more than $1.00 (28%) in the span of two days to a settlement of about $4.84/MMBtu on November 14, the highest price since February 2014, only to whipsaw back down 80 cents the next day. And, since then it hasn’t been unusual to see daily swings of 20-45 cents in either direction. As of yesterday, the now-prompt January 2019 contract was at about $4.34/MMBtu, down 27 cents on the day. The gas market hasn’t seen quite this level of volatility in a decade or more. Why now and what are the fundamentals behind it? With the coldest, highest-demand months still ahead, today’s blog provides an update of the gas supply-demand balance driving the recent price volatility.