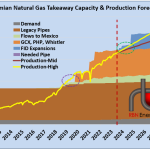

It’s familiar territory for the Permian gas market. Pipeline takeaway capacity constraints are getting worse and will not see any sustained relief for more than a year. To tell this story we’ll use the graph below, which compares Permian pipeline takeaway capacity to Permian production – effectively the call on that capacity.

The bad ole days were in 2019, when Permian gas was severely pipeline constrained (purple dashed circle on graph). In that year, the Price at Waha spent a total of 31 days below zero – that’s the price, not the basis. Gulf Coast Express (GCX) the first of three new pipelines (orange area) came online late that year which helped, followed by PHP (Permian Highway Pipeline) and Whistler. In 2020 the number of days that the Waha price dropped below zero fell to only 9, and when production fell due to COVID that year, 2021 and most of 2022 were zero price free.

But by year-end 2022, constraints were back again (green dashed oval). The price at Waha dropped below zero four times thus far in 2023. And the Waha price this year has averaged $1.47/MMbtu, or 61% of the $2.40/MMbtu average price at Henry Hub.

Relief is coming (blue area), but not soon enough. The WhiteWater/MPLX-Whistler Expansion is scheduled to come online in the next three months, increasing capacity on that pipe by 500 MMcf/d to 2.5 Bcf/d. In the fourth quarter the Kinder/Kinetik/Exxon-PHP Expansion brings another 550 MMcf/d online to boost that pipe’s capacity to 2.6 Bcf/d. But it will be the third quarter of 2024 before the WhiteWater/EnLink/Devon/MPLX- Matterhorn Express Pipeline starts up 2.5 Bcf/d of capacity.

If production increases at the trajectory of our Mid case, that should be enough capacity to get us to 2028. But if our high production case were to happen, then capacity would be constrained again by 2026. Either way, more pipelines will be needed after Matterhorn. The only question is when.