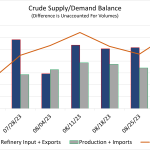

West Texas Intermediate (WTI) and Brent prices rebounded last week to finish at their highest level so far this year amid constrained supplies and stronger economic forecasts, both domestic and foreign. U.S. crude production and refinery input were flat last week, while imports rose to 6.7 MMb/d and exports soared by 400 Mb/d to 4.9 MMb/d. The rise in exports is suspicious as we’d expect volumes to decrease as Hurricane Idalia would have disrupted shipping traffic as it barreled into Florida last week. This increase is likely the reason for the rise in unaccounted volumes, which rose by 900 Mb/d. Finally, West Coast refining demand bounced back after it dipped two weeks ago due to Hurricane Hilary. Imports fell by 700 Mb/d, prompting a 1.4-MMbbl draw on inventories in PADD 5.

Featured Articles

U.S. Gulf Coast Crude Oil Exports Drop to Lowest Level in Over a Year, Partly Driven by Hurricane Francine

Strangers In the Night - WTI and Brent Come Close Enough to Touch

The Brent premium to WTI has traded as wide as $23/Bbl this year but was down to 2 cnts/Bbl on Friday July 19, 2013. At one point during trading nearby WTI prices rose above Brent – the first time that’s happened in three years. Yesterday (July 22, 2013) WTI August expired at 106.91 - $1.14 lower than Brent September. Today we look at why the spread has narrowed so rapidly and whether it will stay that way.

The Rise and Fall of Crude Supply - Shale Crude Production, Inventories and Imports

It looks like a combination of shale crude oil production and inventory drawdowns have been backing out crude oil imports over the past two months. Gulf Coast refineries are leading the way to crank up utilization, increase diesel exports and pull crude oil inventories down from the stratosphere. A lot of this activity seems to be bypassing Cushing. Meanwhile the Gulf Coast is at the center of two big events this week – a tropical storm and a huge refinery fire. Today we continue our analysis of crude inventories.