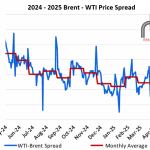

The Brent-WTI spread (July-versus-July contracts) narrowed once again last week, constricting to $3.33/bbl (far right of red line on chart below) - the tightest the spread has been since mid-January (excluding days of Brent expiration when price swings are commonly seen). This Brent-WTI spread (also called “the arb”) represents the price difference between Brent (the global crude benchmark) and CME / NYMEX WTI (the U.S. crude benchmark representing Domestic Sweet Cushing).

Featured Articles

- Blog

Rolling In The Spread? How The Brent/WTI Crude Futures Relationship Got Trickier

In January 2016 the ICE futures Exchange changed the expiration calendar for its flagship Brent crude contract. The March 2016 contract expired on January 29, 2016 under new calendar rules that stipulate expiration one month and one day prior to delivery. This was done belatedly to reflect a change in the assessment of the physical Brent market that was implemented back in January 2012. On paper the change is just an overdue action by ICE to properly align the timing calendar for their popular futures contract with the underlying physical market. But in practice - as we suggest in today’s blog, the change has significant impacts on the calculation and analysis of the commonly utilized spread between ICE Brent (the international benchmark crude) and the U.S. equivalent West Texas Intermediate (WTI) crude futures contract traded on the CME/NYMEX.

- Blog

Tank House Blues – Brent, WTI and LLS Learning to Live With A Crude Oil Glut

In spite of a brief respite provided last week by increased geopolitical risk in Saudi Arabia, crude oil prices are still in the $50/Bbl range – down more than 50% since last Summer - and inventories at Cushing and on the Gulf Coast continue at record levels. The fall in crude prices was initially consistent across markets with international benchmark Brent trading within $1/Bbl of U.S. benchmark West Texas Intermediate (WTI) and Gulf Coast marker Light Louisiana Sweet (LLS) in January 2015. But since February the relationship between Brent, WTI and LLS has changed as the build up of Cushing inventories weighs on prices in the Midwest. Today we provide an update on crude price differentials at The Gulf Coast.

- Blog

Are They Never Ever Getting Back Together Again? Latest WTI/Brent Relationship Update

The West Texas Intermediate (WTI) discount to Brent has narrowed 30 percent in 2013 to close at $13.95/Bbl on Friday March 22, 2013. At the same time Gulf Coast Light Louisiana Sweet (LLS) prices have moved unexpectedly to a $6.75/Bbl premium over Brent. Is the WTI discount to Brent finally unwinding? If so – then why are LLS prices trading above Brent? Today we update our analysis of the WTI/Brent spread.