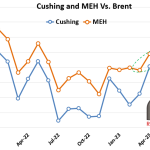

For decades the most watched differentials in crude oil markets has been the spread between North Sea Brent and NYMEX Domestic Sweet or DSW (aka, WTI) at Cushing, OK. But that may be changing since it is now possible to deliver Midland WTI cargos shipped from terminals on the Gulf Coast into the Brent Complex via transport to Rotterdam.

In the graphic below, the blue line is the difference between NYMEX DSW at Cushing versus Brent, with the contract months aligned apples-to-apples. That means if the front month for Brent is September, we compare that price to September NYMEX, regardless of the NYMEX front month (for example, we compare September to September a week ago, even when the NYMEX front month was August).

While the differential between NYMEX DSW versus Brent has been generally narrowing, there has not been a clear trend.

In contrast, the trend for Brent versus MEH is clear and getting quite narrow (orange line). From nearly $6/bbl in November of last year, the differential narrowed to $4/bbl in December, hung there for four months, then shifted to the $3/bbl range in April, narrowing slightly since. The trend has been in part due to declining freight rates, which vary considerably but have generally been trending lower over the past few months. The big question is whether the ability to deliver cargos of Midland WTI into Brent has narrowed the differential permanently, with the exception of periods when something goes crazy with freight rates. Stay tuned. We’ll be watching that differential carefully.